How to create your own Risk Free Capital Protection product?

This one is for you if you are afraid to lose money in the stock market. A capital protection plan is a low risk strategy that will help a new investor get this ‘feet wet’. After all, there is no replacement to hands-on personal experience, and stock investing is no different.

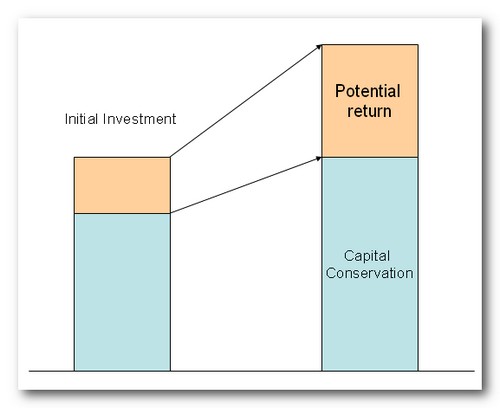

So, what is a structured product? A structured product guarantees that your principal will be protected regardless of the market situation. The upside is usually pegged to NIFTY or SENSEX. This enables an investor to participate in a rally in the stock market while ensuring that there will not be a loss if NIFTY goes down.

Hence it is a great way for new investors to try investing in the stock market with no downside loss.

The downside of such products offered by banks and mutual funds like RelianceMoney are as follows:

Capital Protection – An Investment Option

- They’re not very transparent – They are complicated and not very easy to understand. Some of these products may offer a good balance of risk versus reward, but they’re invariably sold to people who can’t really tell.

- They’re expensive – Not just in terms of the profit you give up for potential security of capital (which may be fair enough) but also the hidden fees rolled into their arcane structure.

- They’re inherently flawed – Most give you a return based on the value of the stock market on some particular day, or if you’re lucky over the average of a few months. But stock markets are volatile, so ill-suited to this.

- The ticket price is pretty high – Generally, these products are sold to high networth individuals.

- Investment is locked for a certain duration – Typically these plans are for a fixed duration. If there is an option to get out of it before the tenure ends, it usually is pretty expensive.

Capital Protection and Gain from Stock Appreciation

People are drawn to these products as the urge for capital protection is strong, rightly or wrongly.

Here’s a very simple way to create your own capital protection plan and gain from the stock market at the same time. It addresses most of the issues mentioned above.

- It is very transparent because you know how you have designed it.

- It may not be much cheaper than the ones offered by professional investors, but you will know exactly where and how much it costs you.

- The returns can be as of any day you choose. You are not locked into a long term investment.

- The ticket price can be as big or small as you please. But to be meaningful, the investment should be at least Rs. 1-2 Lakhs at the minimum.

- Same as # 3. You are not locked in, and can liquidate the NIFTY linked component whenever you wish.

Here’s how. So simple and so sweet!

Your capital protection plan includes two parts:

Part A: Sufficient cash in a fixed rate savings

This is the component that guarantees you get your capital back. Out of your lump sum investment, you put enough cash into this product so that when the compound interest is rolled up you’re left with the same lump sum that you started with. This can be bank FD for 3-5 years, company deposits or debentures, bonds issued by Indian railways or SBI etc.

Part B: Invest the rest in an index fund

The money left over goes into NIFTY BEES. Your total return will be based on the performance of NIFTY over the duration you picked.

Let’s look at an example –

Principal: Rs. 5,00,000

Duration: 3 years

Part A: The cash component

Mahindra Finance offers an interest rate of about 10%. According to the calculator on their website, if you invest Rs. 3,76,000 for 3 years, the cumulative return at the end of the term will be a little over Rs. 5,00,000.

This investment guarantees that you will get your principal back at the end of 3 years.

Part B: Investing the rest in NIFTY Index Fund

Invest the rest of money, that is, Rs. 5,00,000 – Rs. 3,76,000 = Rs. 1,24,000 in NIFTY Index fund. There are at least 15 to choose from. Their annual maintenance charge varies from 0.25% to 1.50%.

Here’s a few examples of how your returns could pan out, depending on how the stock market performs over the three-year period.

| NIFTY Return after 3 Years | -25% | 0% | 25% | 50% | 75% |

| Cash Deposit | Rs. 5,00,000 | Rs. 5,00,000 | Rs. 5,00,000 | Rs. 5,00,000 | Rs. 5,00,000 |

| Index Fund | Rs. 93,000 | Rs. 1,24,000 | Rs. 1,55,000 | Rs. 1,86,000 | Rs. 2,17,000 |

| Net Return | Rs. 5,93,000 | Rs. 6,24,000 | Rs. 6,55,000 | Rs. 6,86,000 | Rs. 7,17,000 |

| Net Return (%) | 18.6% | 24.8% | 31% | 37.2% | 43.4% |

Even if NIFTY returns negative 25%, you will have a net gain of 18.6%.

In fact, if NIFTY goes to zero, and your index fund goes to zero, you’d still get your principal back.

On the other hand, if NIFTY doubles, you make less than half that rise with a 43.5% gain. The cash is a drag on your returns.

In my book, ‘Stock Picking Made Easy’, you will find a simple strategy to identify great companies at reasonable valuations in the Indian Stock Exchange. Identifying great companies at the right time is the key to long term wealth creation.